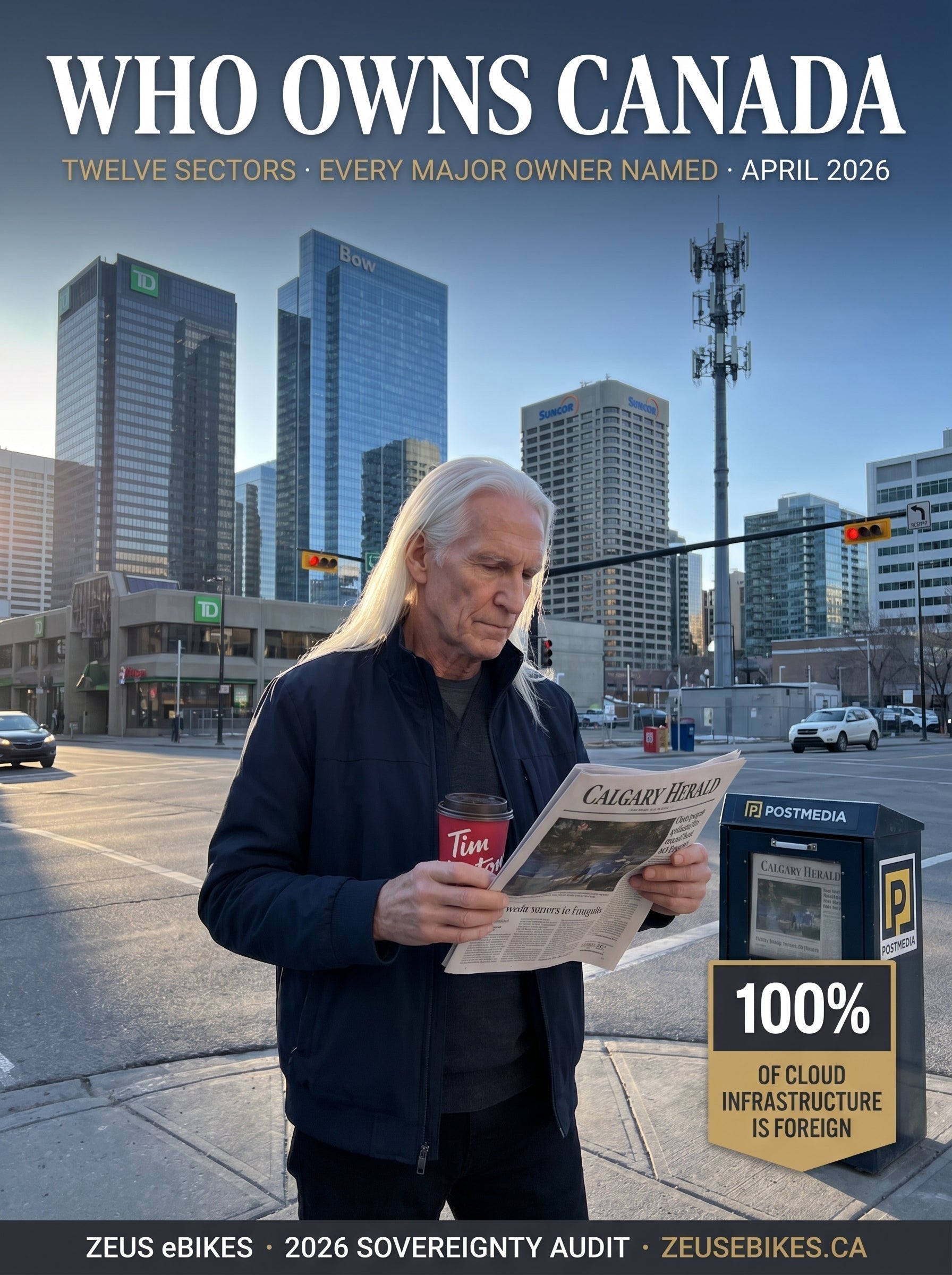

Who Owns Canada? A Name-by-Name Audit of Every Foreign-Held Asset in the Country

Twelve sectors. Every major foreign owner named. The audit Canada never published — and the law that explains why.

in Canada (CAD)

Is American

Audited

Two Foreign Firms

Outflow (Est.)

Since 1985

Canadians own less of their country than they think. US companies alone hold $697.3 billion in Canadian assets — 45.5% of all foreign direct investment (Statistics Canada, 2024). ExxonMobil owns 69.6% of Imperial Oil (per Imperial Oil’s annual disclosures and ExxonMobil’s SEC filings). A US hedge fund controls Canada’s largest newspaper chain. Two foreign companies process an estimated 70–80% of Canadian beef (industry analyses). Virtually all Canadian credit card transactions route through American-owned Visa and Mastercard; Canadian-owned Interac is the lone domestic payment rail. All three hyperscale cloud providers are American.

This is the audit. Twelve sectors. Every major foreign-owned asset named. The pattern is consistent: Canada protected what it wrote rules for. Everything else was sold while no one was watching.

In This Audit

- Why This Audit Exists — The Cargill Question

- The Sovereignty Timeline 1985–2026

- The Ownership Map — All 12 Sectors at a Glance

- 1. Oil, Gas & Pipelines

- 2. Mining & Critical Minerals

- 3. Agriculture, Food & Grocery

- 4. Telecommunications

- 5. Technology & Cloud Infrastructure

- 6. Media & Entertainment

- 7. Banking & Financial Services

- 8. Payment Infrastructure

- 9. Real Estate & Farmland

- 10. Transportation & Infrastructure

- 11. Healthcare & Pharmaceuticals

- 12. Water & Utilities

- The Ownership Scorecard with Vulnerability Heatmap

- International Comparison — Australia, UK, France, Canada

- What Leaves Canada Each Year — The $40–60B Estimate

- The Gatekeeper — The Investment Canada Act

- Accountability — Who Could Change This

- What This Audit Cannot See

- What This Means

- FAQ — Nine Questions, Answered With Names

1. Why This Audit Exists — The Cargill Question

On April 20, 2020, Canada’s largest beef plant went dark.

The Cargill facility in High River, Alberta — a single building forty minutes south of Calgary — processes roughly thirty-six percent of all the beef Canadians eat. By the third week of April, 950 of its roughly 2,200 workers had tested positive for COVID-19. Two were dead. A third worker, the husband of an employee, would die in May. The plant closed on April 20. Canadian beef supply dropped by nearly forty percent inside seventy-two hours.

The plant is owned by Cargill Inc., a privately held American company controlled by the Cargill-MacMillan family. Most Canadians who eat its beef have never heard the name.

What that single shutdown made visible was a question the country had not been asking. One building, foreign-owned, holding more than a third of a national protein supply. If a single facility could do that to beef — what else looked the same?

This audit is the answer to that question. It is not an argument against foreign investment, which has built much of what Canada now owns. It is an inventory: every major sector, every major owner, named.

Cargill High River, 06:18 AM, mid-April. One witness. One building. Thirty-six percent of a country’s beef supply.

Two readings of the same fact set are possible. The first: foreign capital integrated Canada into the global economy, transferred technology, and built infrastructure Canadian capital alone could not have. The second: the concentration of foreign ownership in specific sectors, where no domestic ownership rule exists, has created leverage that can be used against Canadian interests during a crisis. Both readings are defensible. The audit below is the record both readings require.

The pattern that emerges from twelve sectors of forensic ownership data is consistent and uncomfortable: Canada protected what it wrote rules for. Everything else was sold while no one was watching. The five sectors with the highest foreign control share one feature — none have ownership protections equivalent to banking or telecom. The five with the lowest foreign control share the opposite feature.

That is the thesis of this document. The next 9,000 words are the evidence.

2. The Sovereignty Timeline 1985–2026

Twelve dated decisions across forty years produced the 2026 ownership map. The Investment Canada Act was passed in 1985 to screen foreign acquisitions. It was used to block one major deal (BHP/Potash, 2010). The other eleven events on the timeline are the deals that went through, the assets that were nationalised, and the moments that revealed the leverage.

Map 1 — Forty Years of Canadian Ownership Decisions

Three eras, one direction. The Investment Canada Act was used to block once in forty years. The shape of Canadian ownership in 2026 was set in eighteen months across 2006–07.

Sudbury, late April, 14:30. The descendant standing where Inco used to be. Eighteen months in 2006–07 took most of it.

3. The Ownership Map — All 12 Sectors at a Glance

Foreign control across the twelve sectors of the Canadian economy ranges from near-zero (water and utilities) to effectively one hundred percent (cloud, social media, payment networks). The bar chart below shows the gradient. The full sector-by-sector tour follows immediately after.

Map 2 — Foreign Control by Sector, Canada 2026

The gradient is the story. The five most foreign-controlled sectors share one feature: no Canadian ownership rules apply to them. The five least foreign-controlled share the opposite.

| Sector | Foreign Control Level | Key Foreign Owners | Protected by Law? |

|---|---|---|---|

| 1. Oil & Gas | ~25–30% of extraction | ExxonMobil, CNOOC, US institutional investors | Investment Canada Act (post-2013) |

| 2. Mining | ~40–50% of assets | Rio Tinto (UK-AU), Vale (Brazil), Glencore (Swiss) | Investment Canada Act (case-by-case) |

| 3. Food & Grocery | ~70–80% of beef processing | Cargill (US), JBS (Brazil), 3G Capital (Brazil) | No ownership limits |

| 4. Telecom | Legally capped at 20–46.7% | US institutional investors (non-voting) | Telecommunications Act |

| 5. Technology & Cloud | 100% of hyperscale cloud | AWS, Microsoft, Google | No ownership limits |

| 6. Media | Largest newspaper chain | Chatham Asset Mgmt (US hedge fund) | Broadcasting Act (broadcast only) |

| 7. Banking | ~15–25% institutional | Vanguard, BlackRock, State Street (non-voting) | Bank Act (20% single-entity cap) |

| 8. Payments | ~95%+ | Visa, Mastercard, Stripe, PayPal | No ownership limits |

| 9. Real Estate | ~3.5% residential (BC), variable commercial | US institutional, DP World (UAE) | Foreign buyer ban (residential, to 2027) |

| 10. Transportation | Variable — key assets foreign | Ferrovial (Spain), Moroun family (US), DP World (UAE) | Canada Marine Act (ports) |

| 11. Healthcare | ~68–70% of drugs imported | Pfizer, Merck, Roche, AstraZeneca, Teva | No ownership limits on pharma |

| 12. Water & Utilities | Minimal — Crown corp dominated | Hydro One partially public (47.3% provincial) | Provincial Crown corps + legislation |

Now to the names.

4. Oil, Gas & Pipelines — Who Owns Canada’s Energy

Canada is the world’s fourth-largest oil producer and the source of 60% of US crude oil imports. Who owns the companies that pump it?

The Oil Sands — Producer by Producer

| Company | Controlling/Major Owner | Country | Notes |

|---|---|---|---|

| Imperial Oil | ExxonMobil — 69.6% | US | The clearest case of direct foreign control of a major Canadian oil producer |

| Suncor Energy | Widely held. Vanguard, BlackRock, Capital Group each ~5–8% | Mixed (US institutional) | Canadian-headquartered, TSX/NYSE |

| Canadian Natural Resources (CNRL) | Widely held. Vanguard, BlackRock, Fidelity hold major blocks | Mixed (US institutional) | Largest crude oil producer in Canada |

| Cenovus Energy | Widely held. Former CK Hutchison/Li Ka-shing stake reduced post-Husky merger | Mixed | Post-Husky merger (2021) |

| Nexen (CNOOC Ltd) | CNOOC — 100% | China | Acquired for $15.1B (2013). Largest Chinese acquisition of a Canadian company. Triggered the SOE ban |

Athabasca lease, 19:48, mid-April. The Canadian watching what gets pumped from where he sits. The profit goes elsewhere.

Overall: Statistics Canada data (2019) indicated approximately 25–30% of oil and gas extraction assets were foreign-controlled — down from ~37% in 2007, largely because the CNOOC/Nexen deal triggered a policy shift that effectively banned future state-owned enterprise acquisitions of oil sands companies.

The shift matters: direct foreign control decreased, but foreign institutional ownership — Vanguard, BlackRock, Capital Group, Fidelity buying shares on the open market — increased. The companies are Canadian-headquartered and Canadian-managed. The shareholders who profit from them are increasingly not.

Map 3 — Oil Sands Major Producer Composition

The wedge that moves is the green one. Direct foreign control fell after 2013 (CNOOC ban). The US-institutional wedge replaced it. The companies are still Canadian. The dividends are increasingly not.

The Pipelines

| Pipeline | Owner | Country | Notes |

|---|---|---|---|

| Trans Mountain | Government of Canada | Canada | Purchased from Kinder Morgan (US) for $4.5B in 2018. Sale process underway |

| Enbridge | Widely held (TSX/NYSE) | Mixed (US institutional) | North America’s largest pipeline operator |

| TC Energy | Widely held (TSX/NYSE) | Mixed (US institutional) | Spun off South Bow (liquids pipelines) in 2024 |

| Keystone XL | — | — | Cancelled by TC Energy in 2021 after Biden revoked the permit |

Canada nationalised Trans Mountain by buying it from a US company — the rare case of sovereignty flowing the right direction. The pipeline expansion was completed in 2024. Whether the government sells it (and to whom) will determine whether that sovereignty gain is permanent.

5. Mining & Critical Minerals — The $56 Billion That Left in Eighteen Months

Mining is where the biggest foreign acquisitions happened — and where the biggest one was stopped.

| Company | Owner/Acquirer | Country | What They Got |

|---|---|---|---|

| Alcan (now Rio Tinto Alcan) | Rio Tinto — acquired for $38.1B USD (~$41.4B CAD) in 2007 | UK/Australia | Aluminum smelters, iron ore, diamonds. Canada’s largest mining acquisition loss |

| Inco (now Vale Canada) | Vale — acquired for $17.6B USD (~$19.4B CAD) in 2006 | Brazil | Sudbury, Thompson, Voisey’s Bay nickel operations |

| Falconbridge (now Glencore) | Xstrata/Glencore — acquired (2006) | Switzerland | Nickel (Sudbury, Raglan Mine), copper, zinc operations across Canada |

| Teck Resources (coal division) | Glencore — acquired for ~$9B (2024) | Switzerland | Steelmaking coal business. Teck retained copper/zinc |

| Potash Corp (now Nutrien) | BHP hostile bid — BLOCKED ($39B, 2010) | Australia (withdrawn) | The landmark case. Federal government issued a "no net benefit" determination under the Investment Canada Act; BHP withdrew the bid before formal denial |

| Nutrien | Widely held (TSX/NYSE) | Canadian-HQ | Formed from PotashCorp + Agrium merger (2018) |

| Barrick Gold | Widely held (TSX/NYSE) | Canadian-HQ | World’s second-largest gold miner |

| Cameco | Widely held (TSX/NYSE) | Canadian-HQ | Canada’s largest uranium producer. World’s second-largest |

Sudbury Superstack, 20:24, mid-April. The descendant looking up at the monument. Brazilian-owned since 2006.

Overall: Statistics Canada estimates 40–50% of Canadian mining assets are foreign-controlled — significantly higher than oil and gas. The difference is structural: the Investment Canada Act caught the oil sands problem after CNOOC/Nexen, but the mining losses (Alcan, Inco, Falconbridge) happened before the rules tightened.

2006–2007 was the year Canada lost its mining sovereignty. In eighteen months, three of Canada’s most iconic mining companies — Alcan, Inco, and Falconbridge — were acquired by foreign multinationals. The two largest deals (Alcan/Rio Tinto at $38.1B USD and Inco/Vale at $17.6B USD) totalled approximately $56 billion USD combined; the Xstrata/Falconbridge acquisition added approximately another $24 billion USD to the eighteen-month sweep. The industrial capacity, the management talent, the R&D, and the profit streams left with them.

The one that was stopped — BHP’s $39 billion bid for Potash Corp in 2010 — proved the Investment Canada Act could work. Saskatchewan Premier Brad Wall argued potash was a strategic resource. The federal government issued a “no net benefit” determination under the ICA; BHP withdrew the bid shortly after. Potash stayed Canadian.

6. Agriculture, Food & Grocery — Who Feeds Canada

The three companies that control Canadian grocery — Loblaw, Sobeys, and Metro — are Canadian. That is where the good news ends.

The Grocery Oligopoly — Canadian-Controlled

- Loblaw Companies: Controlled by George Weston Ltd and the Weston family (Canadian). Largest grocery retailer.

- Sobeys (Empire Company): Controlled by the Sobey family (Canadian). Second-largest grocery retailer.

- Metro Inc.: Widely held, Canadian-headquartered. Third-largest.

Together they control approximately 60% of Canadian grocery retail. They are Canadian-owned. They are also the subject of an ongoing Competition Bureau investigation into bread price-fixing (Loblaw admitted participation) and sustained public anger over grocery inflation.

The Beef Duopoly — Foreign-Controlled

This is the number most Canadians do not know:

Cargill (US, privately held by the Cargill-MacMillan family — among America’s wealthiest dynasties) operates Canada’s largest beef processing plant in High River, Alberta. It processes roughly 36% of all Canadian beef.

JBS (Brazil, publicly traded, Batista family) owns operations in Brooks, Alberta.

Together, Cargill and JBS control an estimated 70–80% of Canadian beef processing. Two foreign companies. One American, one Brazilian. Processing the vast majority of beef Canadians eat.

Tim Hortons counter, 07:45. The Canadian transaction. The Brazilian owner.

Map 4 — Beef Processing in Canada, By Owner Country

One bar. Three colours. The amber third is American. The red third is Brazilian. The green third is everyone else.

During COVID-19, outbreaks at the Cargill High River plant (over 900 workers infected, 2 deaths) forced the plant to shut down — and Canadian beef supply dropped by nearly 40% overnight. A single foreign-owned facility’s closure caused a national food security crisis. That is the original Cargill question this audit is built around.

Tim Hortons — The Symbol

Tim Hortons, the cultural institution that bills itself as Canada’s coffee shop, is owned by Restaurant Brands International (RBI). RBI is majority-controlled by 3G Capital, a Brazilian private equity firm known for its zero-based budgeting and cost-discipline approach (documented in Tim Hortons franchisee disputes from 2017–2019). 3G Capital also controls Burger King and Popeyes through RBI. Tim Hortons is TSX/NYSE-listed and headquartered in Toronto — but the controlling interest is Brazilian.

The Import Dependency

Canada imports 54.8% of its agricultural products from the US (Agriculture Canada, 2024). During winter months, when domestic production is dormant, an estimated ~90% of leafy greens consumed in Canada are imported, mostly from California and Arizona. 50% of fruit, nut, and vegetable imports by value come from the US.

The Cargill question, returning. One building in High River, Alberta. 950 workers infected. Two dead. Thirty-six percent of national supply offline in seventy-two hours. The plant reopened in May 2020. The question it raised did not.

7. Telecommunications — The Protected Sector

Telecom is one of the few sectors where Canadian law explicitly limits foreign ownership. The Telecommunications Act caps it at:

- 20% direct foreign ownership of a licensed carrier’s voting shares

- 33.3% indirect (through a holding company)

- 46.7% effective combined maximum

The Big 3

Rogers Communications: The Rogers family controls ~97% of voting shares through a dual-class structure. Canadian-controlled regardless of who holds non-voting equity.

BCE (Bell): ~80% institutionally held. US investors (Vanguard, BlackRock) hold substantial non-voting positions. Voting control remains Canadian-compliant.

Telus: Similar pattern — ~75–80% institutionally held. US institutional investors hold significant non-voting stakes.

Southern Saskatchewan, 06:30. The Canadian at the foot of the protected sector. Sovereignty as deliberate policy.

Canadian telecom is legally Canadian-controlled. The capital — the money that profits from some of the highest telecom prices in the developed world — flows substantially to foreign institutional shareholders through non-voting equity.

Internet backbone: Canada’s fibre backbone is primarily Bell, Telus, and regional carriers (SaskTel, Videotron). Zayo Group (US) operates significant fibre in Canada. International undersea cables involve US entities — Canada has only 2 trans-Atlantic fibre optic cables versus 25 landing in the US (CIGI).

8. Technology & Cloud Infrastructure — The Unprotected Sector

If telecom is the sector Canada chose to protect, technology is the one it did not.

What Canada Lost

| Canadian Company | Acquirer | Country | Amount | Year |

|---|---|---|---|---|

| Nortel Networks | Patents sold to Apple, Microsoft, Sony, others | US/Japan | $4.5B USD (patents only) | 2011 |

| ATI Technologies | AMD | US | $5.4B USD | 2006 |

| Slack (Canadian founder Stewart Butterfield) | Salesforce | US | $27.7B USD | 2021 |

| Hootsuite | Meltwater | Norway | Undisclosed | 2024 |

Nortel alone was worth $250 billion CAD at peak — one-third of the entire Toronto Stock Exchange. Its collapse — which followed a decade-long network intrusion widely reported to involve China-based attackers, exposed publicly by former Nortel security advisor Brian Shields in 2012, with estimates of exfiltrated R&D ranging from $20–30 billion — is documented in our annexation investigation. The patents were sold. The talent dispersed. The building became DND headquarters.

Foreign AI Labs on Canadian Soil

Canada’s AI talent — concentrated at the Vector Institute (Toronto), Mila (Montreal), and the Alberta Machine Intelligence Institute — is increasingly employed by foreign companies operating Canadian labs:

- Google DeepMind — Toronto

- Meta FAIR — Montreal (recruited from Yoshua Bengio’s lab)

- Samsung AI Centre — Toronto and Montreal

- LG AI Research — Toronto

- Nvidia — Toronto

- Microsoft Research — Montreal

Suburban Montreal, 11:30, mid-April. The Canadian at the fence. The data is on his soil. The servers are not.

Cloud Infrastructure — 100% Foreign

All three hyperscale cloud providers operating in Canada are American: AWS (Amazon) — Montreal, Calgary regions; Microsoft Azure — Toronto, Quebec City regions; Google Cloud — Montreal, Toronto regions.

Per Shared Services Canada’s Cloud Brokering vendor framework, 7 of the 8 federally-listed cloud providers are US-headquartered. The single Canadian-owned provider is ThinkOn. There is no Canadian-owned hyperscale cloud infrastructure. When a Canadian company says “your data is stored in Canada,” it typically means a US company’s server in a Canadian data centre — subject to the U.S. CLOUD Act.

No ownership limits. No Investment Canada Act intervention at scale. No foreign ownership caps. The result: 100% of hyperscale cloud is foreign. 100% of AI lab employment by foreign companies produces foreign-owned IP. Nortel’s $250 billion in value was lost permanently. ATI, Slack, and Hootsuite were acquired. Shopify and OpenText survive — protected not by law but by founder share structures. Technology is the sector where Canada most clearly chose market openness over sovereignty.

9. Media & Entertainment — Who Controls What Canadians Read

Newspapers — The Chatham Problem

Postmedia Network is Canada’s largest newspaper chain. It publishes the National Post, Vancouver Sun, Ottawa Citizen, Calgary Herald, Edmonton Journal, Montreal Gazette, and dozens of regional papers. Its controlling interest is held by Chatham Asset Management, a US hedge fund run by Anthony Melchiorre. Chatham acquired control through debt restructuring — converting debt to equity. Canada’s most influential newspaper chain answers to a New Jersey hedge fund.

Torstar (Toronto Star): Acquired by NordStar Capital in 2020. Canadian-controlled. The Globe and Mail: Owned by the Thomson family through Woodbridge Company. Canadian-controlled.

Downtown corner, 06:15. The Canadian picking up his paper. The hedge fund picking up his subscription dollars.

Broadcasting — Protected

The Broadcasting Act requires Canadian control of broadcasters — 80% of voting shares and 80% of board directors must be Canadian. Bell Media (CTV, Crave), Rogers (Citytv, Sportsnet), Corus (Global) — all Canadian-controlled. The Broadcasting Act works for broadcasting.

It does not work for streaming. Netflix reaches 70% of Canadians vs Crave’s 23%. Netflix, Disney+, Amazon Prime, and Apple TV+ have no obligation to carry any specific percentage of Canadian content — only a 5% revenue contribution to Canadian production funds, which is currently being challenged in court.

The 100% Block — Three Sectors with No Canadian Voice

Three categories of digital infrastructure are effectively 100% foreign-owned. They are the three with the least public regulation. They are also the three with the most direct daily impact on Canadian life.

Hyperscale Cloud

100%Microsoft Azure (US)

Google Cloud (US)

Canadian alternative: ThinkOn (small, not hyperscale)

Payment Networks

~95%Mastercard (US)

Stripe (US/Irish-American)

PayPal (US) · Square (US)

Apple Pay · Google Pay (US)

Canadian alternative: Interac (single rail)

Social & Streaming

100%Google (YouTube, US)

TikTok (ByteDance, China)

X / Twitter (US)

Netflix · Disney+ · Apple TV+ (US)

Canadian alternative: none at scale

10. Banking & Financial Services — The Fortress

Canadian banking is the best-protected sector in the country. The Bank Act limits any single entity to 20% of voting shares for Schedule I banks. No single foreign entity can control a major Canadian bank.

The Big 5 — RBC, TD, BMO, Scotiabank, CIBC — are all Canadian-headquartered and Canadian-managed. Their boards are majority-Canadian. Their strategic decisions are made in Toronto.

But.

US institutional investors — Vanguard, BlackRock, and State Street — collectively hold an estimated 15–25% of Big 5 shares across all classes (per recent 13F filings; the figure varies bank-to-bank and quarter-to-quarter). No single entity exceeds 20%. But the aggregate foreign institutional ownership of Canada’s banking system is substantial.

Bay Street, 06:55, mid-April. The citizen at the foot of the fortress. The fortress holds. The shareholders are increasingly elsewhere.

These are passive index-fund holdings — not strategic control. Vanguard does not tell RBC how to lend. But the profit flows. Canadian banks generated record profits during a period of housing unaffordability and consumer debt crisis. A meaningful share of those record profits went to foreign shareholders.

Insurance: Canadian-domiciled insurers (Manulife, Sun Life) compete with foreign-owned operators including Aviva (UK), AIG (US), Zurich (Switzerland), and Allianz (Germany). Desjardins is a Canadian cooperative.

11. Payment Infrastructure — The Invisible 100%

This is the sector most Canadians have never thought about. It is also effectively 100% foreign-controlled.

Every time a Canadian swipes a credit card or pays online, the transaction routes through American-owned infrastructure. The exception is debit on the Interac network — the only major payment rail in Canada that is Canadian-controlled. Everything else — Visa, Mastercard, Stripe, PayPal, Square, Apple Pay, Google Pay — is American.

Coffee counter, 09:15. The single most unconscious transaction in Canadian daily life. American the entire way through.

The Tap of a Card — What One Coffee Transaction Touches

One $4 coffee at Tim Hortons. Six layers of infrastructure. Four foreign owners traversed in under a second.

The Tap, Decomposed

Six layers. Four foreign-owned. The only consistently Canadian touchpoint is the bank that settles the funds — and even there, USD-denominated transactions route through a US correspondent bank, creating jurisdictional exposure to US law.

12. Real Estate & Farmland — What They Own, What They Don’t

Statistics Canada’s Canadian Housing Statistics Program (2020) found foreign owners held approximately 3.5% of residential properties in BC and 2.2% in Ontario. In Vancouver condos specifically, foreign ownership reached ~7.6%.

The Prohibition on the Purchase of Residential Property by Non-Canadians Act (2023, extended to 2027) and the Underused Housing Tax (1% annually on vacant/underused foreign-owned residential properties) have reduced new foreign purchases to near-zero.

Foreign ownership of Canadian residential real estate is a real issue but a smaller one than public perception suggests. The housing crisis is driven primarily by domestic factors — supply constraints, zoning, interest rates, and population growth — not foreign buyers.

False Creek seawall, 20:38, mid-April. The resident at the city most cited as the foreign-buyer story. The data tells a smaller one.

Commercial — Less Transparent

Major Canadian commercial REITs (RioCan, Allied, Choice Properties) are publicly traded with significant US institutional shareholders (BlackRock, Vanguard, State Street) holding 5–15% stakes through index funds. Brookfield Asset Management is Canadian-headquartered. Oxford Properties (OMERS) is Canadian pension-controlled.

There is no central database tracking total foreign ownership of Canadian commercial real estate. This is a transparency gap — one of the areas where this audit cannot provide a definitive number because the data does not exist in a publicly accessible form.

Farmland — Province-by-Province Restrictions

Saskatchewan restricts non-resident ownership of farmland. Alberta and Manitoba have varying restrictions. PEI caps individual holdings at 1,000 acres for non-residents. No national database of foreign-owned farmland exists.

13. Transportation & Infrastructure — The Assets You Cross Every Day

Rail

CN Rail and CPKC are TSX/NYSE-listed and Canadian-headquartered. But their shareholder bases tell a different story:

- CN: TCI Fund Management (UK, Chris Hohn) held ~5–6%. Cascade Investment (Bill Gates) held ~10% historically. BlackRock, Vanguard among the largest holders.

- CPKC: Similarly major US institutional holders.

Highway 407 — The $3.1 Billion Lesson

In 1999, Ontario sold the Highway 407 Express Toll Route on a 99-year lease for $3.1 billion. Current ownership: CPP Investments (Canadian) ~50.01%; Cintra/Ferrovial (Spain) ~43.23%; SNC-Lavalin/AtkinsRéalis (Canadian) ~6.76%.

Highway 407, 20:15, mid-April. Ninety-nine-year lease. Forty-three percent Spanish-controlled. He pays each time he crosses.

The highway has generated tens of billions in toll revenue since. The sale is widely regarded as one of the worst public asset dispositions in Canadian history.

The Ambassador Bridge — Privately Owned by an American

The Ambassador Bridge connecting Windsor, Ontario to Detroit, Michigan is privately owned by the Moroun family (Detroit, USA). It is the only major privately owned international crossing between Canada and the US. The Gordie Howe International Bridge (opened 2024) was built partly to reduce Canadian dependency on a single privately owned US-controlled border crossing.

Ports

Vancouver Fraser Port Authority, Montreal Port Authority, and Halifax Port Authority are federal Crown corporations. The ports themselves are Canadian. Terminal operators within them may not be: DP World (UAE, state-owned by Dubai) operates container terminals at Vancouver’s Centerm and Montreal’s Termont.

Airports

Canadian airports are operated by non-profit Canadian airport authorities on federal Crown land leases. Not foreign-owned. Not privately held. This is one sector Canada got structurally right.

14. Healthcare & Pharmaceuticals — The Supply Chain Vulnerability

Canadian healthcare delivery is public. The pharmaceutical supply chain that feeds it is not. Canada imports approximately 68–70% of its pharmaceutical products. The US is the largest source, followed by the EU.

The major pharmaceutical companies operating in Canada are all foreign: Pfizer (US), Merck (US), Johnson & Johnson (US), AbbVie (US), Roche (Switzerland), Novartis (Switzerland), Sanofi (France), AstraZeneca (UK/Sweden), GSK (UK), Bayer (Germany), Teva (Israel).

Canadian generic manufacturers Apotex and Pharmascience are privately held and Canadian-controlled. They represent a fraction of total pharmaceutical supply.

Pharmacy aisle, 11:00, mid-April. Every box at eye level is foreign-owned. He needs every one of them.

Canada imports ~85% of its medical devices, primarily from the US (~60% of device imports), followed by Germany, Japan, and China.

15. Water & Utilities — The Last Fortress

This is the good news sector.

BC Hydro, Hydro-Québec, Manitoba Hydro, SaskPower — all provincial Crown corporations. Publicly owned. Not for sale.

Ontario Power Generation: Provincial Crown corporation (generation). Hydro One (transmission and distribution) was partially privatised in 2015 — it is publicly traded (TSX) with the province retaining ~47.3% and a legislated 40% cap on foreign ownership.

Municipal water treatment and distribution remain municipally operated across Canada. No verified examples of foreign-owned Canadian municipal water systems exist.

Manic-5, 17:45, mid-April. No human in the frame. Public ownership at full scale. The counterpoint to every other photo in the audit.

Water and electricity are the sectors where Canada most fully maintained public ownership. The Crown corporation model — provincially owned, self-financing, and constitutionally protected — has prevented the privatisation that affected utilities in the UK, Australia, and parts of Europe.

16. The Ownership Scorecard with Vulnerability Heatmap

| Sector | Canadian Control | Foreign Control | Legal Protection | Vulnerability |

|---|---|---|---|---|

| Water & Utilities | Very High | Minimal | Crown corps + legislation | Low |

| Banking | High | ~15–25% institutional | Bank Act (20% cap) | Low |

| Telecom | High (voting control) | Significant non-voting equity | Telecommunications Act | Low |

| Broadcasting | High | Minimal (domestic broadcasters) | Broadcasting Act | Low |

| Airports | High | None | Crown land leases | Low |

| Long-Term Care | High | Minimal | Provincial regulation | Low |

| Ports | High (ownership) | DP World operates terminals | Canada Marine Act | Medium |

| Oil & Gas | Medium | ~25–30% + ExxonMobil/Imperial | Investment Canada Act (post-2013) | Medium |

| Real Estate | Medium–High | ~3.5% residential, variable commercial | Foreign buyer ban (residential) | Medium |

| Rail | Medium (management) | Substantial institutional | None specific | Medium |

| Mining | Low–Medium | ~40–50% | Investment Canada Act (case-by-case) | High |

| Newspapers | Mixed | Largest chain US hedge fund-controlled | None | High |

| Food Processing (Beef) | Low | ~70–80% (Cargill + JBS) | None | Critical |

| Streaming & Social Media | None | 100% | None meaningful | Critical |

| Pharmaceuticals | Low | ~68–70% imported | None on ownership | Critical |

| Cloud Infrastructure | None (hyperscale) | 100% | None | Critical |

| Payment Infrastructure | Interac only | ~95%+ | None | Critical |

| Technology (general) | Low | Major acquisitions + AI labs | None specific | Critical |

Where Canada has ownership laws — banking, telecom, broadcasting, utilities — Canadian control is preserved. Where Canada has no ownership laws — food processing, payments, cloud, technology, newspapers, streaming, pharmaceuticals — foreign control ranges from substantial to total. Six sectors carry a Critical vulnerability rating. None of those six have ownership protections equivalent to banking or telecom.

17. International Comparison — How Other Democracies Do It

Canada is not alone in confronting the question of foreign ownership in a globalised economy. Three peer democracies — Australia, the United Kingdom, and France — operate explicit screening regimes for foreign investment. Their frameworks are structurally comparable to Canada’s Investment Canada Act. Their application is not.

Map 5 — Foreign Investment Screening, Four Countries

The frameworks look similar. The application does not. Australia, UK, and France use their screening tools regularly. Canada has formally rejected one major bid in forty years.

Three observations from the comparison.

First, Canada has the broadest sector list on paper. The 2024 ICA expansion added 31 sensitive business sectors triggering mandatory national security review. That is more sectors than the UK’s 17 NSIA categories or France’s 11 strategic sectors. The legislative coverage is comprehensive.

Second, Canada uses the tool least often. Australia’s FIRB has formally blocked or conditionally rejected multiple major foreign acquisitions per year for decades. The UK’s NSIA, in force since 2022, has issued approximately 20 blocking or conditional orders. France has used its sector framework actively since the 2005 PepsiCo/Danone deterrent. Canada has formally rejected one major acquisition under the ICA in forty years — BHP/Potash, 2010, on net benefit grounds, after which BHP withdrew the bid.

Third, the contrast matters because the assets at stake are comparable. Australia’s blocked Hong Kong/Ausgrid deal (2016) involved electrical grid infrastructure of similar national importance to Canadian utilities. The UK’s blocked Newport Wafer Fab acquisition (2022) involved semiconductor capacity comparable to what Nortel once represented for Canada. The tools exist. The political will to use them does not appear to. That is a choice, not an inevitability.

18. What Leaves Canada Each Year — The $40–60 Billion Estimate

How much foreign profit leaves Canada annually from named Canadian assets? Statistics Canada publishes total investment income paid to non-residents in its Balance of International Payments (Table 36-10-0014-01), which captures dividends, interest, and reinvested earnings flowing to foreign owners across both direct and portfolio investment — the most recent annual figures are in the $80–120 billion range. The narrower question this audit asks — what foreign profit specifically attributable to the named direct-ownership stakes documented above leaves Canada each year — is not reported as a single figure. The estimate below derives that subset.

It is the order of magnitude this audit can defend with public data.

Map 6 — Estimated Annual Foreign Profit Outflow by Sector (CAD)

$40–60 billion a year leaves the country. Oil and gas alone is the largest outflow channel. The estimate is conservative — the actual number is almost certainly higher.

For perspective: $40–60 billion per year is approximately equal to the 2024 federal deficit ($40 billion projected). It is roughly 1.5–2.5x annual federal Canada Health Transfer payments to provinces. It is the recurring cost of foreign ownership in Canadian assets, paid every year, in addition to whatever profits the assets generate for their Canadian operations and whatever taxes they pay.

This narrower direct-FDI subset does not appear in federal budget documents or election platforms. The audit produces this specific cut because no other source breaks it out at the sector level.

19. The Gatekeeper — The Investment Canada Act

The Investment Canada Act (1985) is the federal law that reviews foreign acquisitions of Canadian businesses above a threshold value (currently ~$1.141 billion for private-sector WTO investors). Reviews assess “net benefit to Canada.”

Track record:

- BHP/Potash Corp (2010): BLOCKED — $39 billion hostile bid. The federal government issued a "no net benefit" determination under the Investment Canada Act; BHP withdrew the bid before formal denial. The landmark case.

- CNOOC/Nexen (2013): APPROVED — but triggered a policy shift: future SOE acquisitions of oil sands companies would only be approved on an “exceptional basis.”

- Alcan/Rio Tinto (2007): APPROVED. $38.1 billion.

- Inco/Vale (2006): APPROVED. $17.6 billion.

- Falconbridge/Xstrata (2006): APPROVED.

- Glencore/Teck coal (2024): APPROVED. $9 billion.

The Act was strengthened in 2009 (national security review added) and 2024 (expanded critical minerals protections, 31 sensitive business sectors). It now includes mandatory national security filing for investments in those sectors.

But the Act cannot undo the past. Alcan, Inco, and Falconbridge are gone. The roughly $80 billion USD in combined mining assets that left in 2006–2007 (Alcan + Inco + Falconbridge) are not coming back. The Act is stronger now than it was then. Whether it is strong enough for what comes next — AI acquisitions, data sovereignty, critical mineral processing — remains an open question.

20. Accountability — Who Could Change This

The decisions documented in this audit were made by named people in named roles. The decisions that could change the future are also made by named people in named roles. The accountability is not abstract.

Who currently holds the levers:

- The Minister of Innovation, Science and Industry — primary federal authority over the Investment Canada Act. Reviews and decides on foreign acquisitions above the threshold. The 2010 BHP/Potash decision was made by then-Minister Tony Clement under Prime Minister Stephen Harper.

- The Minister of Finance — controls Bank Act enforcement, OSFI direction, and the broader regulatory framework for foreign investment in financial services.

- The Minister of Public Safety — co-signs national security reviews under the ICA when the security trigger is invoked.

- The Standing Committee on Industry and Technology (INDU) — House of Commons committee with jurisdiction over the Investment Canada Act. Holds hearings on foreign-acquisition policy. Last major ICA review hearings: 2024.

- The Office of the Commissioner of Canada Elections — relevant for foreign-owned media’s influence on Canadian elections, but with narrow enforcement scope under the Canada Elections Act.

What would have to change to extend ownership protections to the unprotected sectors:

- An amendment to the Telecommunications Act or a new sector-specific framework to apply ownership caps to data infrastructure (cloud, payments) the way the Bank Act applies them to deposit-taking institutions.

- An expansion of the Broadcasting Act Canadian-content and Canadian-control provisions to streaming services and major social platforms operating in Canada (the Online Streaming Act, S.C. 2023, c. 8 was a partial step; enforcement is in progress).

- A new Food Sovereignty Act or amendment to the Investment Canada Act creating a statutory ownership cap for food-processing facilities above a national-supply-share threshold (e.g., any single facility processing more than 20% of national supply for a given protein category triggers Canadian-control requirements).

- Establishment of a federal beneficial ownership registry for Canadian corporations (the Canada Business Corporations Act amendments of 2023 created this for federally-incorporated companies; provincial alignment is incomplete).

- Active use of the existing Investment Canada Act national security review in the 31 sensitive sectors added in 2024. The legislative authority exists. The political application has not.

None of the five changes above is technically difficult. All five are politically difficult. The constraint is not law-drafting capacity. The constraint is the willingness of any government to apply the tools the legislative framework already provides.

21. What This Audit Cannot See

Forensic ownership work runs into the limits of public data. The honest version of this audit names what it cannot see, in addition to what it can.

Commercial real estate. No central federal database tracks foreign ownership of Canadian commercial real estate. Provincial land title registries record individual transactions but no federal aggregation has been published. Foreign institutional holdings in Canadian commercial REITs are reportable on a quarterly basis but not aggregated into a sector-wide foreign-ownership figure. The audit can name BlackRock and Vanguard’s 5–15% stakes in major REITs. The audit cannot name the share of total Canadian commercial real estate value that is foreign-controlled.

Farmland. Saskatchewan, Manitoba, Alberta, and PEI maintain provincial restrictions on non-resident farmland ownership, with provincial enforcement records. No federal aggregation exists. National foreign-ownership share of Canadian agricultural land is not measured.

Beneficial ownership behind shell companies. The federal beneficial ownership registry under the Canada Business Corporations Act became operational in 2024 for federally-incorporated companies only. Provincial beneficial ownership registries are at varying stages of implementation. Numbered companies and trust structures still mask ultimate beneficial ownership in many cases. The audit can name the listed corporate owner. The audit cannot always name the ultimate beneficial owner behind that listed corporate owner.

Privately-held foreign multinationals. Cargill is privately held. Its Canadian operating financials are not publicly disclosed. The 36% beef-share figure cited in this audit comes from public industry reporting and Cargill’s own corporate communications, not from audited financial statements. The same caveat applies to other privately-held foreign companies operating in Canada.

Intra-firm transfer pricing. When AWS Canadian region serves a Canadian government customer, the revenue may be booked to AWS Inc. in the United States rather than to a Canadian subsidiary, depending on the contractual structure. The economic activity occurs on Canadian soil. The recorded financial activity may not. Federal tax data on this is confidential to CRA.

Crown corporation shareholders by individual name. Crown corporations (CN, CPKC pre-1995, etc.) had public shareholder records pre-privatisation. Post-privatisation institutional holdings are tracked at the broker level but individual ultimate beneficial ownership is not typically publicly disclosed below the 10% threshold.

Each of these limits is a transparency gap that public policy could close. The absence of the data is itself a public policy choice.

22. What This Means

This audit reveals a country with a split character.

Protected Canada — banking, telecom, broadcasting, water, utilities, airports — is substantially Canadian-controlled. Ownership laws work. Crown corporations work. The 20% cap on bank ownership works. The Telecommunications Act works. The Broadcasting Act works. Where Canada wrote rules, sovereignty held.

Unprotected Canada — food processing, payments, cloud, technology, newspapers, streaming, pharmaceuticals — is substantially foreign-controlled. No ownership laws exist. No threshold reviews trigger. No cap prevents concentration. Where Canada wrote no rules, market forces produced the predictable result: the larger economy absorbed the smaller one.

The five sectors with the highest foreign control are payment infrastructure (~95%+), cloud infrastructure (100%), streaming and social media (100%), beef processing (70–80%), and pharmaceuticals (68–70% imported). None of these five sectors has ownership protections equivalent to banking or telecom.

The question this audit poses is not “should Canada ban foreign investment.” That would be economically destructive and strategically foolish. The question is: should Canada extend the ownership protections that work in banking, telecom, and utilities to the sectors where they don’t exist — before the next crisis reveals which dependency can be weaponised?

The peer-democracy comparison answers part of that question. Australia, the UK, and France use foreign-investment screening tools regularly and visibly. Canada has the broadest legislative authority on paper and uses it the least often. That is a choice.

The annual outflow estimate — $40–60 billion in foreign profit leaving Canadian assets each year — is the recurring cost of the choice. It is not a hidden number. It is just an unpublished one.

Every name in this audit is a fact. Every ownership percentage is sourced. The question of what to do about it belongs to Canadians — but only if they know the facts first.

The Cargill plant in High River reopened in May 2020. Production resumed. Cargill remains the single largest beef processor in the country. The two workers who died did not come back.

Sovereignty is not a slogan. It is a list of buildings, pipelines, servers, and feedlots, and the names of the people who own them. This is the list. The audit ends here. The decisions about what to do with it belong to Canadians.

Cargill High River, 06:48, mid-April. The plant is open. Production resumed. The witness who started the audit stays to watch the workers arrive.

23. FAQ — Nine Questions, Answered With Names

What percentage of Canada is foreign-owned?

US companies alone hold $697.3 billion CAD — 45.5% of all FDI (Statistics Canada, 2024). Sector-specific control varies: ~25–30% of oil and gas, ~40–50% of mining, 70–80% of beef processing, 68–70% of pharmaceuticals (imported), 100% of payment card networks, 100% of hyperscale cloud, and 100% of social media platforms.

Who owns Canada’s oil sands?

ExxonMobil owns 69.6% of Imperial Oil. CNOOC owns 100% of Nexen ($15.1B, 2013). Suncor, CNRL, and Cenovus are widely held with major US institutional investors (Vanguard, BlackRock, Fidelity).

Who owns Canada’s mines?

Rio Tinto (UK/Australia) acquired Alcan for $38.1B USD / ~$41.4B CAD (2007). Vale (Brazil) owns former Inco nickel operations ($17.6B USD / ~$19.4B CAD, 2006). Glencore (Switzerland) acquired Teck’s coal division ($9B, 2024). BHP’s $39B hostile bid for Potash Corp was rejected in 2010 (no net benefit determination; BHP withdrew). Nutrien, Barrick Gold, and Cameco remain Canadian-headquartered.

How much foreign profit leaves Canada every year?

An order-of-magnitude estimate based on 2024 Statistics Canada FDI inward stocks ($1.53T CAD) at sector-weighted average return on invested capital (4–6%) yields a defensible range of $40–60 billion CAD per year. The bulk concentrates in oil and gas, mining, food processing, technology services, and the institutional dividend share of banking. See the full methodology in Section 18.

Who owns Canada’s grocery stores?

Loblaw (Weston family, Canadian), Sobeys (Sobey family, Canadian), and Metro (widely held, Canadian) control ~60% of grocery retail. All three are Canadian-controlled. But Cargill (US) and JBS (Brazil) control 70–80% of beef processing. Tim Hortons is controlled by 3G Capital (Brazilian).

Who controls Canada’s digital infrastructure?

AWS, Microsoft Azure, and Google Cloud — all American — operate 100% of hyperscale cloud. Visa and Mastercard (US) process virtually all Canadian credit card transactions; Canadian-owned Interac dominates debit. Stripe, PayPal, and Square (US) dominate online payments. Postmedia (largest newspaper chain) is controlled by Chatham Asset Management (US hedge fund). Interac is the single Canadian-controlled payment rail.

Are Canadian banks foreign-owned?

No — the Bank Act caps any single entity at 20% of voting shares. The Big 5 are Canadian-controlled. But Vanguard, BlackRock, and State Street collectively hold an estimated ~15–25% of Big 5 shares (per recent 13F filings; varies bank-to-bank and quarter-to-quarter).

How does Canada compare to Australia, UK, and France on foreign-ownership rules?

Canada has the broadest sector list on paper (31 sensitive sectors under the 2024 ICA expansion). Canada uses the tool least often (one major formal block in 40 years). Australia, UK, and France use their screening tools regularly. The frameworks are structurally comparable. The application is not.

Does foreign ownership of Canada matter?

Foreign investment creates jobs, capital, and integration. The question is concentration and leverage. When two companies control 70–80% of beef, when 100% of payments run through US networks, when the largest newspaper chain answers to a US hedge fund, when all cloud infrastructure is CLOUD Act-exposed — the issue is not ownership per se. It is whether that ownership can be used as leverage during a crisis. The 2025 tariff war and the Cargill High River shutdown both answered that question: it can.

- Will the USA annex Canada? The 12 threats already here — the companion sovereignty investigation

- What happens to Canada if the U.S. stops being our friend — the practical survival guide

- Canada sends $300B/yr to foreign auto companies — the $15/year alternative

- Why buy an electric bike from a Canadian company — 29 picks, $999–$6,299

- Electric bikes Canada (2026) — 16 verified picks across 6 rider types

This audit was researched and written by Milad Ghobadibeygvand, co-founder of Zeus eBikes Canada. The article is built from public filings, regulatory disclosures, and Canadian government statistical tables. No comment was solicited from named entities; every claim cites a primary public source. Corrections to verifiable factual errors are welcomed at editorial@zeusebikes.ca. The article will be re-checked quarterly. Next scheduled review: July 2026.

All photography by Playcut.ai — personalised AI actor technology.

Share:

Canadian eBike Legal Access Atlas 2026: Where You Can Ride, by Bike Type and Province

Best Cargo eBikes Canada (2026): 25 Verified Picks for Hauling Kids, Groceries & Gear